For venture capital investors in the life sciences sector, intellectual property (IP) is not merely a legal checklist item, it can be a primary determinant of company value, competitive insulation, and exit options. Yet IP due diligence in life sciences remains inconsistently performed across the investment community, with many funds either over-relying on patent counsel opinions that lack commercial context or under-investing in IP analysis relative to clinical and scientific review. This article identifies and analyzes the ten most consequential IP issues that venture investors should evaluate when assessing a life sciences portfolio company, with particular attention to how the materiality and risk profile of each issue shifts across financing stages – from pre-seed and seed through Series A, B, and growth-stage rounds.

Introduction

Life sciences venture investment is, at its core, a bet on exclusivity. Whether the asset is a small molecule therapeutic, a biologic, a diagnostic platform, or a medical device, the investment decision at least partially depends on the company’s ability to erect and defend durable barriers to competition. Patents and related IP rights are the primary instruments through which that exclusivity is secured. It follows that a fund’s ability to assess IP with the same rigor it brings to clinical, scientific, and commercial diligence is a genuine competitive advantage.

Despite this, IP review is often treated as a binary pass/fail screen rather than a nuanced, stage-sensitive value analysis. The result is that investors sometimes miss significant upside in companies with undervalued IP estates, and more consequentially sometimes fund companies whose IP positions will not sustain the exclusivity runway required to justify the capital at risk. This framework is designed to address that gap.

The ten issues discussed below are not presented in order of universal priority – their relative importance shifts meaningfully depending on the company’s stage, asset type, and competitive landscape. Stage-specific guidance is embedded throughout.

1. Patent Landscape Position and Freedom to Operate

Freedom to operate (FTO), the ability to commercialize a product without infringing third-party patents, is a threshold issue at virtually every stage. At Series A, it is often the most pressing IP question, particularly for companies entering crowded therapeutic areas or building on broadly licensed platform technologies. Investors should not accept a company’s internal FTO assessment at face value; the analysis should be conducted or reviewed by independent counsel, with explicit attention to blocking patents, design-arounds, and the litigation or licensing history of key patent holders in the space.

At seed and pre-seed stages, a full FTO opinion may not yet exist, but investors should at minimum understand whether the founding team has identified the key third-party patent families in the landscape and whether any obvious blocking rights are present. At growth stage, FTO analysis must extend to key international markets, particularly the EU, China, and Japan.

2. Patent Claim Quality and Scope

Not all patents are equal. A patent with broad, well-drafted claims covering a genus of compounds or a functional mechanism of action is an entirely different asset than one confined to a narrow species or a specific formulation. Investors should evaluate not just whether a company has patents, but what those patents actually claim. Key questions include: Do issued claims cover the product as currently designed? Do they cover the product as competitively relevant alternatives might be designed? Are method-of-treatment claims available to extend protection beyond composition claims?

This issue becomes increasingly important as the company approaches commercialization. At seed stage, pending applications should contain both broad claims and narrow claims covering the specific product; by Series B, investors should expect to see at least some issued claims with meaningful scope, and any significant narrowing during prosecution should be understood and contextualized with an eye towards prosecution history estoppel.

3. Prosecution Status and Continuation Strategy

A well-managed patent prosecution strategy allows a company to pursue additional claim scope, adapt to evolving product definitions, and maintain pendency as a deterrent to competitors. Conversely, a prosecution strategy that has allowed all applications in a family to issue or go abandoned without continuations pending is a significant limitation on future IP optionality.

Investors should evaluate prosecution as a forward-looking matter: are there pending applications that can yield commercially valuable claims? Is the company investing appropriately in prosecution relative to its stage and competitive environment? At growth stage, prosecution activity should be robust, reflecting the company’s deepening understanding of the competitive landscape.

4. Ownership and Chain of Title

Ownership defects are among the most common and potentially most damaging IP problems encountered in early-stage diligence. Common issues include: inventors who never executed assignment agreements; work performed at a prior employer or academic institution giving rise to competing ownership claims; and government rights under the Bayh-Dole Act arising from federally funded research, which can include march-in rights and obligations to license to U.S. manufacturers.

This issue is most critical at seed and pre-seed stage, when the IP estate is being built on a foundation that often includes academic spin-out technology, founder inventions conceived at prior employers, or federally funded research. Title defects discovered late, during Series B diligence or worse, during an acquisition, can be extremely costly to cure and can destroy deal value entirely.

5. Patent Term and Exclusivity Runway

A patent that expires before or shortly after product approval has severely diminished commercial value. Investors must map the expected patent expiration dates of key assets against the projected development and approval timeline. For pharmaceutical and biologic assets, this calculation must account for patent term extension (PTE) under 35 U.S.C. § 156, which can restore up to five years of patent term lost during regulatory review.

At Series A and B, investors should model the realistic exclusivity window, namely patent term plus regulatory exclusivity. A compound with a ten-year development timeline facing patents expiring in twelve years presents a fundamentally different risk profile than one with patents expiring in twenty years.

6. Section 101 Subject Matter Eligibility Risk

Since the Supreme Court’s decisions in Mayo, Alice, and Myriad, subject matter eligibility under 35 U.S.C. § 101 has been a persistent and disproportionate risk for certain categories of life sciences innovation, particularly diagnostics, biomarker-based methods, personalized medicine platforms, and software-enabled healthcare applications. Claims directed to natural phenomena or abstract ideas, without meaningful additional inventive concept, remain vulnerable to § 101 rejection both during prosecution and in litigation.

Investors evaluating diagnostics companies or platform businesses with significant software or algorithm components must treat § 101 eligibility as a primary diligence item, not a secondary legal footnote. The question is not merely whether claims have been allowed, especially since patent examiners are inconsistent on § 101 application, but whether the claims would likely survive a litigation challenge.

7. Post-Grant Validity Exposure

Inter partes review (IPR) and post-grant review (PGR) proceedings before the Patent Trial and Appeal Board (PTAB) have fundamentally altered the risk profile of issued patents. And more recently, ex parte reexmination has had a renewed focus. Investors should assess the vulnerability of key patents to post-grant challenge: Are the claims supported by strong prosecution history? Is the prior art landscape clean? Have similar patents in the space been successfully challenged at PTAB?

This issue is particularly important at later stages, when the company’s patents have become commercially significant enough to attract adversarial attention. A Series C or pre-IPO company should be able to demonstrate that its key patents have been stress-tested against the most relevant prior art.

8. Regulatory Exclusivity Layering

Patent protection and regulatory exclusivity are distinct but complementary mechanisms, and sophisticated IP strategy in life sciences involves optimizing both. Key regulatory exclusivity periods include: five-year new chemical entity (NCE) exclusivity for small molecules; twelve-year reference product exclusivity for biologics under the Biologics Price Competition and Innovation Act (BPCIA); seven-year orphan drug exclusivity; and pediatric exclusivity, which adds six months to existing patent or exclusivity terms.

Investors should evaluate whether the company’s regulatory strategy is aligned with its IP strategy to maximize total exclusivity. A company developing a biologic for a rare disease that qualifies for both orphan drug designation and BPCIA exclusivity, layered on top of composition-of-matter patents, presents a very different exclusivity profile than one relying on a single expiring patent. This analysis is relevant at every stage but becomes a primary commercial diligence item at Series B and beyond.

9. Licensing and Collaboration Analysis

Many life sciences companies are built on in-licensed technology, and the terms of those licenses can be highly consequential for investors and acquirers. Key issues include: field-of-use and territory restrictions that limit commercialization options; milestone and royalty obligations that affect financial projections; sublicensing rights (or restrictions) that constrain partnership and out-licensing strategies; and change-of-control provisions that could trigger termination or renegotiation upon acquisition.

At seed and Series A stage, the primary concern is whether the foundational license from an academic institution or prior company is on commercially workable terms. By growth stage, the full license portfolio must be mapped and modeled, with explicit attention to provisions that could affect exit valuation or structure.

10. International Portfolio Alignment

A patent is a national right, and a company with a strong U.S. patent position but no international coverage has materially limited its commercial optionality in an industry where global partnerships and licensing are central to exit strategy. Investors should evaluate whether the company has filed PCT applications and pursued national phase entry in key jurisdictions, at minimum the EU (via the EPO), China, Japan, and South Korea, and whether the prosecution strategy in those jurisdictions reflects an understanding of local patentability standards.

China and Japan present particular challenges: China’s biosimilar and generic manufacturing landscape makes robust Chinese patents strategically important, while Japanese prosecution often requires specialized claim drafting. EU prosecution under the EPO involves heightened written description and enablement scrutiny relative to U.S. standards. At pre-seed and seed stage, international filings may be appropriately deferred; by Series A, PCT strategy should be in place, and by Series B, national phase entry decisions should have been made with commercial strategy in mind.

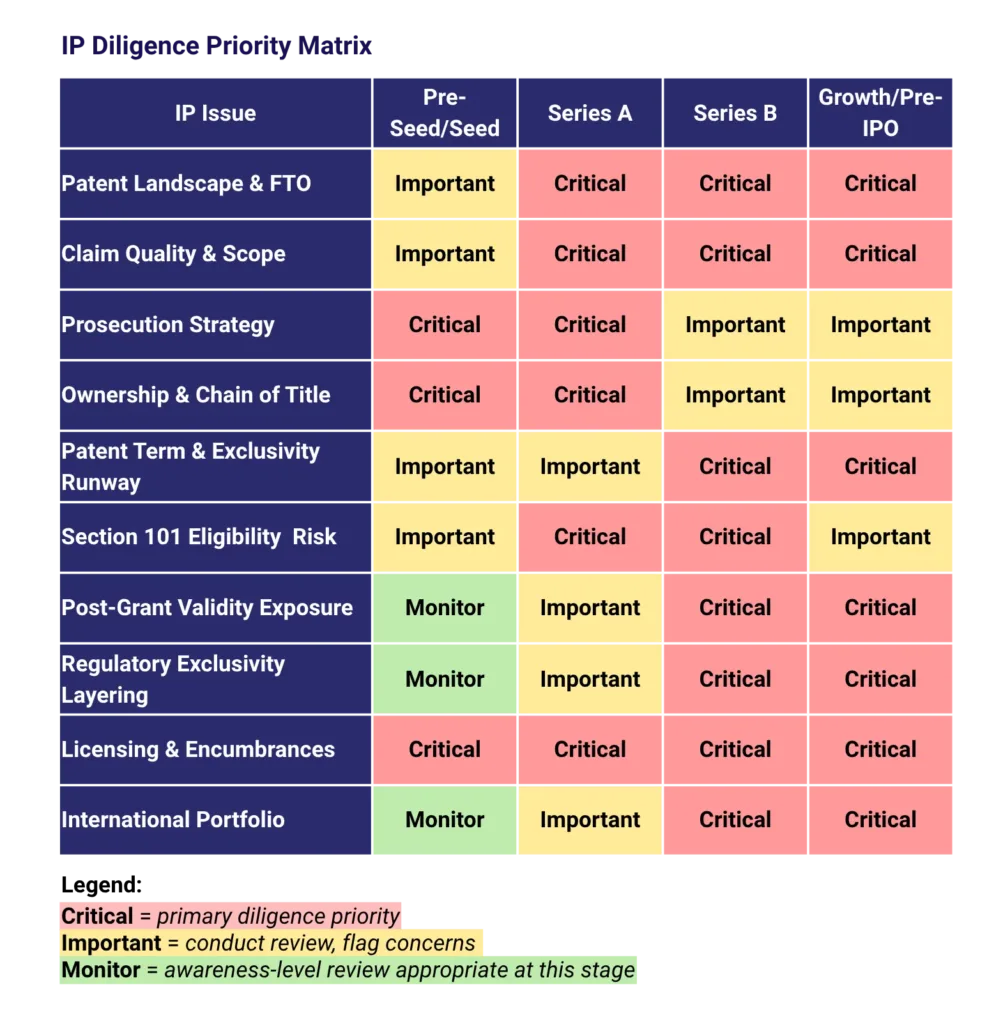

Stage-by-Stage IP Diligence Priority Matrix

The matrix below summarizes the relative priority of each of the ten IP issues across financing stages. Priorities reflect both the likelihood that a defect exists at that stage and the materiality of that defect to investment decision-making and value. Issues rated “Critical” warrant deep independent review; “Important” issues should be reviewed and flagged; “Monitor” issues are worth tracking but typically do not require the same depth of analysis at that stage.

Conclusion: IP Diligence as Investment Discipline

The ten issues outlined above are not a checklist to be completed and filed. They are a framework for ongoing, stage-calibrated analysis with the IP portfolio of a company’s value. At the earliest stages, investors are assessing foundation and optionality: Is the IP estate cleanly owned? Are the right applications being filed with the right claim scope? Is the prosecution strategy coherent? At later stages, the focus shifts to durability and defensibility: Will the exclusivity runway support the investment decision? Are the patents likely to survive challenge? Does the international portfolio support the partnership and exit strategy?

Life sciences venture investors who bring this level of analytical rigor to IP diligence, integrating legal, regulatory, and commercial perspectives, will consistently make better-informed investment decisions and will be better positioned to identify both the hidden risks and the underappreciated value that IP represents in this asset class.

Related Industries

Related Services

Receive insights from the most respected practitioners of IP law, straight to your inbox.

Subscribe for Updates